Has the breakthrough time for tokenization arrived?

Original article by Token Dispatch, Prathik Desai

Original compilation: Block unicorn

preface

Tokenization is booming as Wall Street giants rapidly scale up deployments, a concept that just a few years ago was in beta.

Multiple financial giants are launching platforms, building infrastructure, and creating products at the same time, connecting traditional markets with blockchain technology.

In the last week alone, BlackRock, VanEck, and JP Morgan have made significant moves, demonstrating that tokenization of real-world assets has gone beyond proof-of-concept to become a cornerstone of institutional strategy.

In today's article, we'll show you why the long-awaited inflection point for tokenization may have arrived, and why it still matters even if you've never bought cryptocurrency.

Trillions of potential

"Every stock, every bond, every fund – every asset – can be tokenised. If it happens, it will revolutionise investment," BlackRock CEO and Chairman Larry Fink said in his 2025 annual letter to investors.

Fink was talking about an opportunity that would allow fund companies to tokenise more than a trillion dollars worth of assets in the global asset industry.

Traditional financial giants have seized this opportunity, with a surge in adoption over the past 12 months.

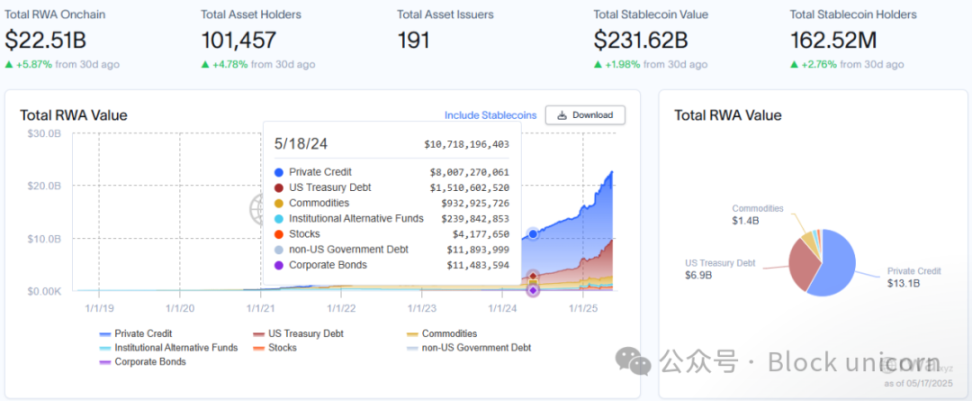

Tokenized real-world assets (RWAs, excluding stablecoins) have surpassed $22 billion, up 40% this year alone. However, this is just the tip of the iceberg.

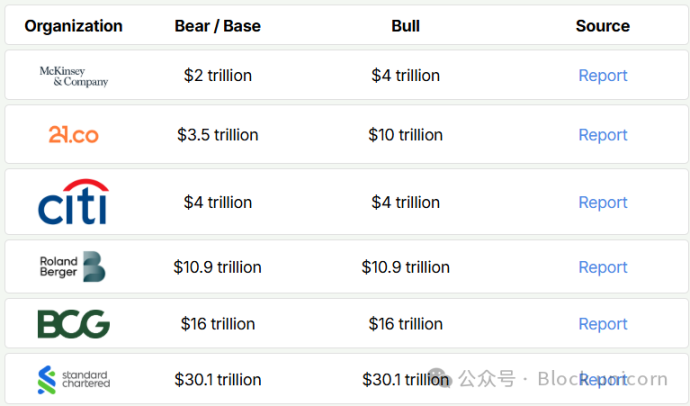

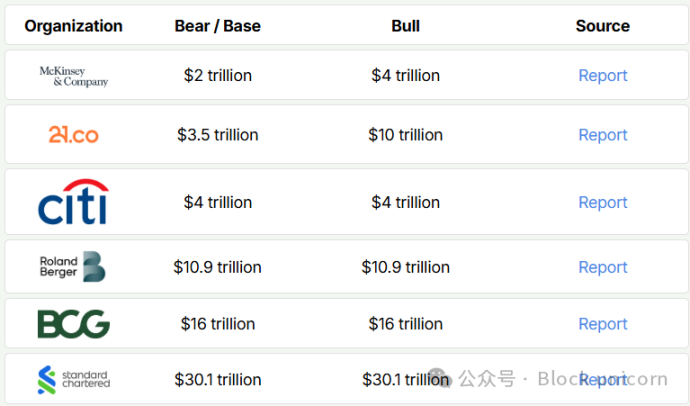

Consulting firm Roland Berger predicts that the tokenised RWA market will reach $10 trillion by 2030, compared to $16.1 trillion estimated by the Boston Consulting Group.

For ease of understanding, even at a lower estimate, this would mean a 500-fold increase over today. If 5% of global financial assets are transferred on-chain, we're talking about a trillion-dollar shift.

Before we explore the fund's tokenization initiatives, let's understand what tokenization is and what it means for investors.

The combination of physical assets and blockchain

Three simple steps: Choose a real-world asset, create a digital token that represents ownership of that asset (in part or in full), and make it tradable on the blockchain. That's tokenization.

The assets themselves (Treasury bonds, real estate, stocks) have not changed. What has changed is the way in which its ownership is recorded and transacted.

Why tokenise? Four key benefits:

-

Fractional ownership: You can own a portion of a commercial building for as little as $100 instead of millions of dollars.

-

Round-the-clock trading: No need to wait for the market to open or settle for liquidation.

-

Reduced costs: Fewer middlemen mean lower fees.

-

Global access: Investment opportunities that were previously geographically restricted are now accessible on a global scale.

"If SWIFT is a postal service, then tokenization is email itself – assets can be transferred directly and instantly, bypassing intermediaries." BlackRock's Fink said in the letter.

Silent revolution

BlackRock's tokenised Treasury bond fund, BUIDL, has surged to $2.87 billion, more than quadrupling in 2025 alone. Franklin Templeton's BENJI holds more than $750 million. JPMorgan Chase's latest move to connect its private blockchain, Kinexys, with the world of public blockchains.

The value of tokenised U.S. Treasuries is now close to $7 billion, up from less than $2 billion a year ago, further confirming this growth story.

More and more giant companies are jumping on the bandwagon with unique products.

This week, VanEck launched a tokenised U.S. Treasury fund accessible on four blockchains, intensifying competition in the rapidly expanding on-chain real-world asset (RWA) market.

Earlier this month, Dubai-based MultiBank Group, the world's largest financial derivatives institution, signed a $3 billion real-world asset (RWA) tokenization agreement with UAE-based real estate giant MAG and blockchain infrastructure provider Mavryk.

Smaller countries are joining the bandwagon. According to the Bangkok Post, the Thai government offers bonds to retail investors through tokenization, with the entry threshold reduced from the traditional $1,000 plus $3 to $3.

Even government agencies did not miss the revolution.

The U.S. Securities and Exchange Commission (SEC) has just hosted a roundtable with nine financial giants to discuss the future of tokenization, which is diametrically opposed to the attitude of previous administrations.

For investors, this means round-the-clock access, near-instant settlement, and fractional ownership.

Think of it as the difference between buying an entire album CD and just streaming the songs you want to listen to. Tokenization splits assets into small, affordable portions, making them accessible to everyone.

Why is it happening now?

-

Regulatory clarity: Under the leadership of U.S. President Donald Trump, his administration has shifted from law enforcement to promoting innovation, with several pro-crypto figures leading government agencies.

-

Institutional adoption: Traditional financial giants provide legitimacy and infrastructure support for tokenization.

-

Mature technology: Blockchain platforms have evolved to meet institutional needs.

-

Market demand: Investors are looking for more efficient and accessible financial products.

U.S. Securities and Exchange Commission (SEC) Chairman Paul Atkins sees tokenization as a natural evolution of financial markets, likening it to "the transition of audio from analogue vinyl to tape to digital software decades ago."

The road ahead

Despite the momentum, challenges remain.

Regulatory fragmentation: The global regulatory landscape remains unified. The SEC's roundtable showed that the United States is open-minded, but international coordination is insufficient. Japan, Singapore, and the European Union are advancing at different paces, and the frameworks are incompatible, which creates compliance challenges for global tokenization platforms.

Lack of standardisation: The industry lacks a unified technical standard for tokenization of different asset classes. Should tokenised treasury bonds on Ethereum be compatible with those on Solana? Who verifies the token's association with the underlying asset? Without standardisation, it is possible to form isolated liquidity pools rather than a unified market.

Custodian and security concerns: Traditional institutions remain cautious about blockchain security. Earlier this year, the $1.4 billion Bybit hack raised tough questions about immutability and recoverability.

The gap in market education: Wall Street may be accelerating, but the general public ("Main Street") still generally lacks understanding of tokenization.

Our point of view

Tokenization could be the bridge that connects blockchain technology with mainstream finance. For those who have followed the evolution of blockchain, this may be the biggest impact in the space to date – not to create new currencies, but to change the way we access and trade the assets we already have.

Most people don't care about blockchain. They care about getting paid earlier, accessing investment opportunities that would otherwise be reserved for the wealthy, and not being squeezed by high fees when moving money. Tokenization provides these benefits without requiring users to understand the underlying technology.

As this space grows, tokenization can become "stealth infrastructure" – like you don't think of the SMTP protocol when you send emails. You'll have easier access to investments with lower fees and fewer restrictions.

Traditional finance has spent centuries developing systems that favour institutions and exclude ordinary people. For decades, we've embraced a financial system designed around institutional convenience rather than human experience. Want to trade after hours? Unfortunately, no. Only $50 to invest? Not worthy of our attention. Want to transfer internationally without losing 7% fees? Then wait slowly.

Tokenization has the potential to break this inequality in just a few years.

With the popularity of tokenised experiences, the conceptual barriers between "traditional finance" and "decentralised finance" will naturally dissolve. People who buy tokenised bonds from the Thai government for $3 may later explore DeFi protocols that can generate yield. Institutional investors who are first exposed to blockchain through BlackRock's BUIDL may end up investing in native crypto assets.

This model drives real application, not through ideological shifts, but through practical advantages, and the old approach is extremely inefficient by comparison.